Students and former students who are at least 90 days late on student loan payments has jumped 3.2 percent in only two years, rising from 8.5 percent in 2011 to 11.7 percent today, according to the New York Federal Reserve, including loans in deferment or in grace periods and therefore temporarily not in the repayment cycle. Excluding such grace period loans, the actual delinquency rate is more than 30 percent – in 2004 it was under 20 percent.

Just for the 2011-12 school year, students and their families borrowed $76 billion to pay for college, according to the Pew Research Center. In sum, Americans owe a total of nearly $1 trillion in student debt broken down as follows:

- 40 million people owe an average of $26,000 after graduation

- 6.8 million Federal student loan borrowers are now in default representing $85 billion

- Most are under 30 who attended for-profit colleges

- 40+ % under 30 have outstanding student loan debt

- 57 % of graduates of for-profit schools owe more than $30,000

- 25 % of graduates from private non-profit colleges owe more than $30,000

- 12 % of public-college graduates owe more than $30,000

- $3.5 billion in government and private student loans went bad in the first three months of 2013

- In 2005, 9% of 25 to 30-year-olds with student debt were granted a mortgage

- In 2012, 4% of 25 to 30-year-olds with student debt were granted a mortgage

The student debt of $1 trillion owed hinders the U.S. economy, says the New York Federal Reserve, by robbing the housing market of its richest crop of new buyers: young college graduates. The implications for the housing market are serious. The majority of first-time home buyers, traditionally aged 25 to 34, has been shrinking since 2008, and young buyers now make up their smallest share of the housing market in more than a decade.

Worse, according to Pew Research Center, these 24-35 year old “millennials” have displaced their home borrowing power, that is, student loans have displaced home loans.

Even worse, by contrast, credit-card debt losses fall on banks and private-sector lenders. But student debt puts taxpayer dollars at risk. After first surpassing credit-card debt in mid-2010, the amount of student-loan debt outstanding has quickly surged to become 42 percent larger than the $674 billion of credit-card debt outstanding.

These negative lending trends impact parents, too. Families are more likely to use retirement savings to fund college. Nearly 6 % of parents now paying for college are drawing on retirement funds either by taking a loan or by withdrawing retirement funds, according to a 2012 Sallie Mae survey. Parents, thus, indirectly are digging the economic hole deeper.

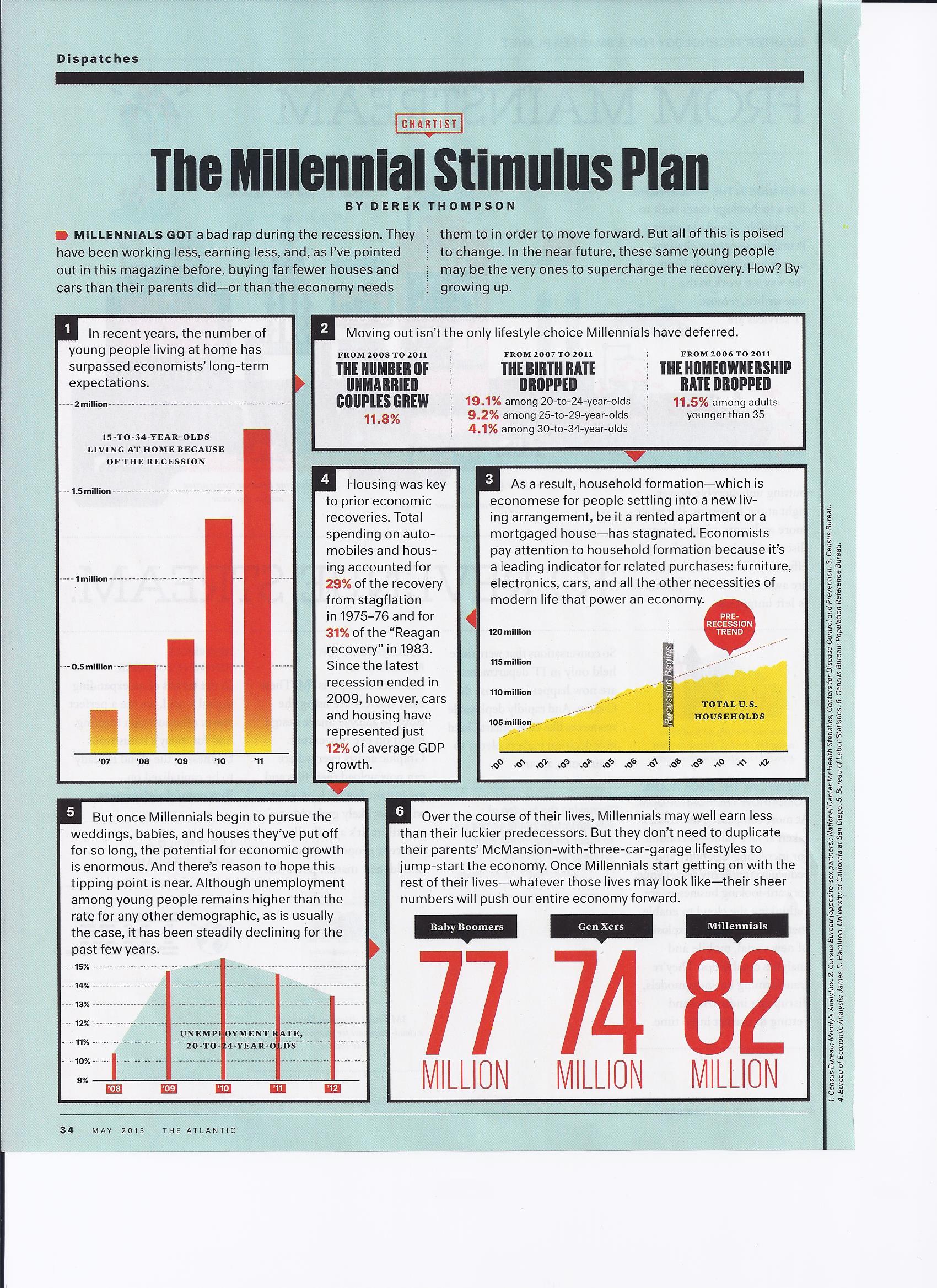

However, wait. Derek Thompson of the Atlantic Monthly sees light at the end of the tunnel:

The Millennial Stimulus Plan

How young people will supercharge the recovery

DEREK THOMPSON APR 24 2013

Millennials got a bad rap during the recession. They have been working less, earning less, and, as I’ve pointed out in this magazine before, buying far fewer houses and cars than their parents did—or than the economy needs them to in order to move forward. But all of this is poised to change. In the near future, these same young people may be the very ones to supercharge the recovery. How? By growing up.